What's the Probability of Loss from an Autocallable Note?

What's the Probability of Loss from an Autocallable Note?

Autocallable structured notes with coupons in the 10%+ range are popular with income-seeking investors. But what's the actual probability that you'll lose money?

We analyzed a real 10.75% p.a. CHF Autocall Barrier Reverse Convertible linked to Bayer, EMS-CHEMIE, and Lonza (worst-of structure) to answer that question.

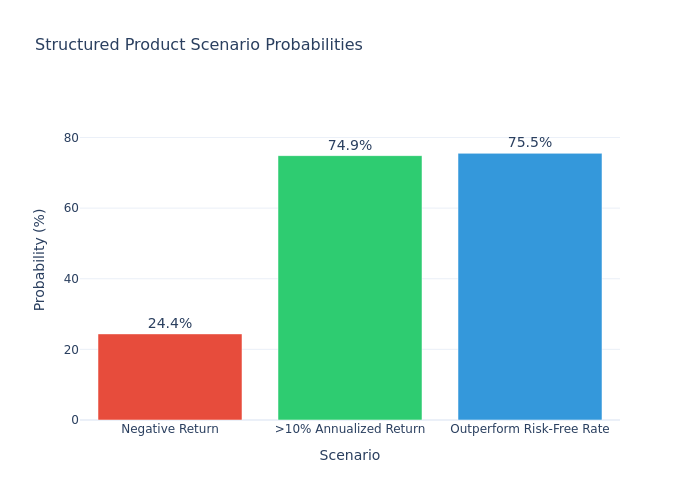

The Probability of Loss: 21.3%

After running a Monte Carlo simulation with 50,000 paths, the probability of a negative total return was 21.3%. That's roughly 1 in 5 — meaning in one out of every five simulated market scenarios, an investor would have ended with less than their initial investment.

Why the Risk Exists

Despite a 10.75% annual coupon, the product carries several risks that can result in losses:

- Barrier risk. If any of the three underlyings falls below the barrier level on an observation date, the conditional protection is lost.

- Worst-of structure. The product tracks the worst-performing of Bayer, EMS-CHEMIE, and Lonza — all three must stay above their barriers for full protection.

- Loss of coupons. In barrier-breach scenarios, not only is principal at risk, but future coupon payments stop as well.

Expected Return vs. Headline Coupon

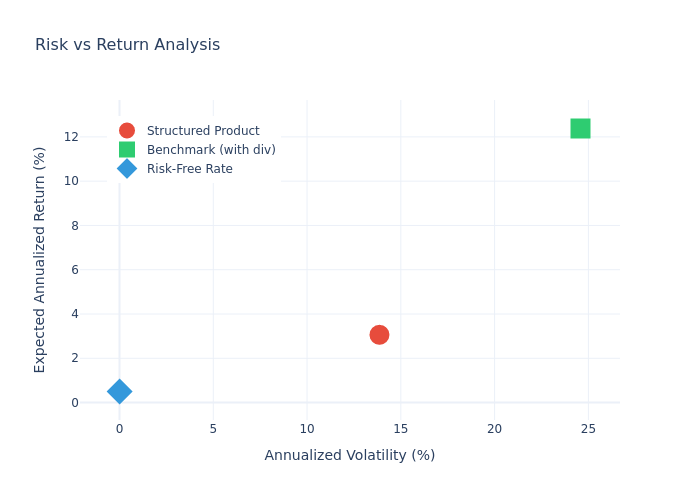

The headline coupon is 10.75% p.a., but the expected annualized return after simulation is only 3.06%. That's a 7.69 percentage point gap — and understanding why is crucial.

The gap exists because:

- In good scenarios, the product autocalls early, capping total return

- In moderate scenarios, coupons may be missed during periods when underlyings dip below the barrier

- In bad scenarios, investors lose both coupons and principal

- In good scenarios, the product autocalls early, capping total return

- In moderate scenarios, coupons may be missed during periods when underlyings dip below the barrier

- In bad scenarios, investors lose both coupons and principal

How Autocall Probability Affects Returns

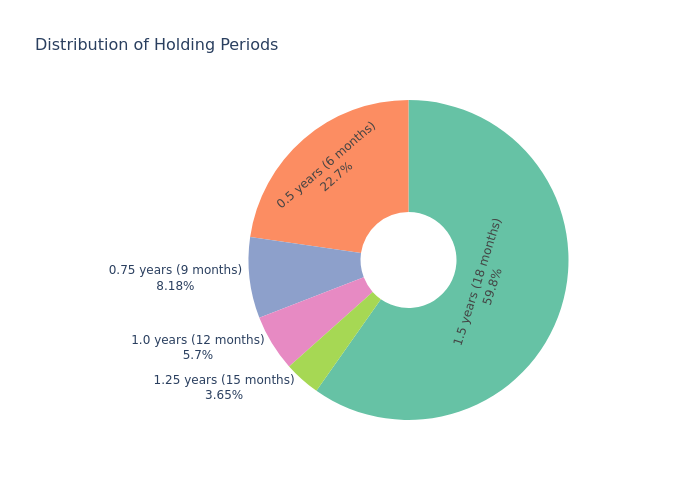

Our simulation found a ~35% probability that the product gets called early in the first year alone. Early call means you receive your coupon plus principal back, but lose the opportunity to earn future coupons — reducing total return vs. holding to full maturity.

Key Takeaway

An autocallable with a 10.75% coupon has a ~1 in 5 chance of losing money. The expected return is far below the headline coupon. Always run a simulation to understand the real probability distribution — not just the best-case scenario.

Run a full Monte Carlo simulation on any autocallable note with Token Engine's SP Evaluator. See the true probability of loss before you invest.