What's the Average Return from a 13% Coupon Structured Product?

What's the Average Return from a 13% Coupon Structured Product?

A 13% p.a. coupon looks attractive on paper. But the expected return — the average outcome after running 50,000 simulations — is often significantly lower. Here's why.

The Real-World Example: A Multi Barrier Reverse Convertible

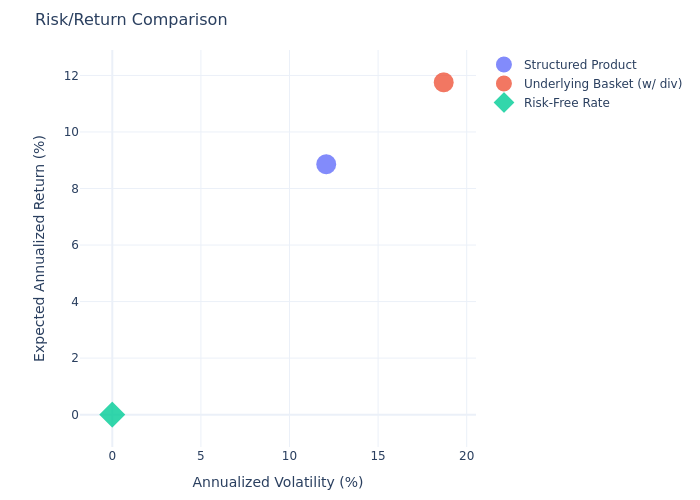

We analyzed a 13.00% p.a. Multi Barrier Reverse Convertible linked to Roche Holding, Sandoz Group, and VAT Group (worst-of structure). The headline coupon: 13% paid quarterly. But the expected annualized return came out at just 8.86%.

How can a 13% coupon product only return 8.86% on average?

The Gap Explained

Three factors eat into that headline 13%:

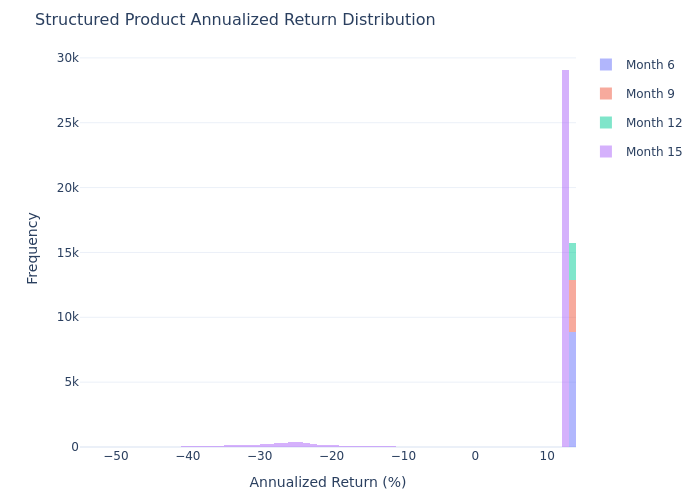

1. Barrier risk. If any of the three underlying stocks falls below 70% of its initial level, the conditional downside protection is lost and investors are exposed to losses on the worst-performing stock. Our simulation found a 10.64% barrier breach probability.

2. Early call probability. The issuer can call the product early. Our simulation found a 31.42% probability of early call within the first year, which caps the total coupon income.

3. Coupon loss on barrier breach. When the barrier is breached, investors stop receiving coupons and instead receive shares worth less than their initial investment.

The Full Picture

The product successfully reduces volatility and downside risk compared to holding the underlying basket directly, but it also caps the upside at 13% minus whatever losses occur in barrier-breach scenarios.

Key Takeaway

A high coupon is not the same as a high return. Always look at the expected return, probability of negative return, and barrier breach probability — not just the headline coupon rate.

Use Token Engine's SP Evaluator to run a full Monte Carlo simulation on any structured product, revealing the true expected return behind the coupon.