Can a High-Coupon Structured Product Still Lose Money?

Can a High-Coupon Structured Product Still Lose Money?

Yes. A high coupon does not guarantee a positive return. In fact, some of the highest-coupon structured products also carry the highest downside risk. Here's a data-driven look at what actually happens in the worst-case scenarios.

The Paradox of High Coupons

The highest headline coupons often come from products with the most aggressive structures:

- Barrier Reverse Convertibles — high coupons but significant barrier risk

- Worst-of structures — high coupons but concentrated risk on the worst-performing asset

- Low barriers — more likely to be breached, triggering principal losses

Case Study 1: A 13% Coupon Product That Can Still Lose

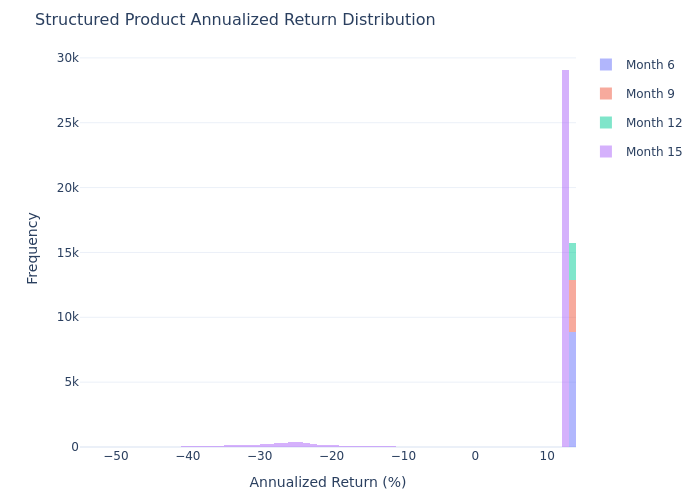

The 13.00% p.a. Multi Barrier Reverse Convertible linked to Roche, Sandoz, and VAT Group pays a generous 13% coupon quarterly. But the 50,000-path Monte Carlo simulation reveals a 10.36% probability of negative total return.

In the worst 1% of scenarios, investors lose −36.11% (99% VaR).

The histogram shows the full picture: while most outcomes cluster in positive territory (thanks to the high coupon in non-breach scenarios), there is a distinct left tail where the barrier is breached and investors suffer significant losses.

What drives the loss? If any of the three underlying stocks falls below 70% of its initial level, the conditional downside protection is voided. Investors receive shares in the worst-performing stock — worth substantially less than their initial investment. The 13% coupon is never enough to offset a 30%+ decline in the underlying.

Case Study 2: 10.75% Coupon, 21% Loss Probability

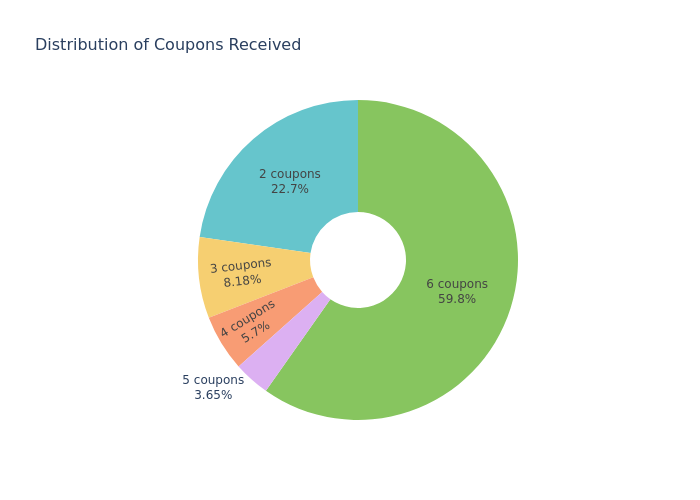

The 10.75% p.a. CHF Autocall on Bayer, EMS-CHEMIE, and Lonza tells a similar story. Despite the high quarterly coupon:

The coupon distribution chart shows that while 60% of paths receive all 6 coupons, the remaining 40% receive fewer — either because of early autocall (which caps total coupon income) or because the autocall barrier is never triggered and the product runs to maturity with risk of loss.

- Probability of negative return: ~24% — nearly 1 in 4 chance of losing money

- Expected annualized return: 3.06% — far below the 10.75% headline

- 99% VaR: −35.59% — worst-case losses comparable to holding the underlying basket

Why the Coupon Doesn't Protect You

Here's the key insight: when the barrier is breached, the coupon stops mattering.

A 13% coupon over 15 months totals approximately 16.25% of principal. That is generous — but a single barrier breach can wipe out 30%+ of capital. The coupon is conditional income, not downside protection.

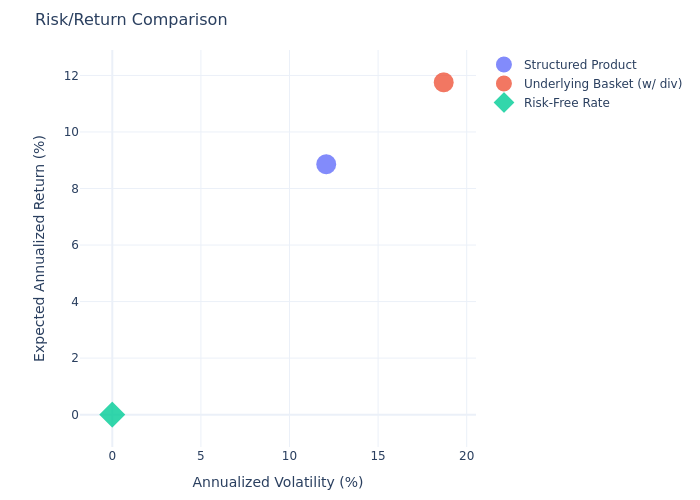

What the Risk/Reward Comparison Shows

The scatter plot compares the structured product against holding the underlying basket directly. The product has lower variance and a higher expected return in most scenarios — but it still carries a left tail where losses exceed −20%. The coupon cushions some losses but cannot eliminate the tail risk inherent in barrier-based structures.

Key Takeaway

High coupon ≠ low risk. In fact, products with the highest headline coupons often have the most risk because:

A 10-13% coupon might look like easy money, but the data shows a 10-24% probability of loss and worst-case losses exceeding −35%. Always run a Monte Carlo simulation before investing: the headline coupon is the best case, not the expected outcome.

Upload a term sheet → Token Engine's SP Evaluator shows the full distribution of returns, not just the best case.