tokenengine.ai

Structured Product Evaluator |

info@tokenengine.ai

Structured Product Analysis Report

Headline Simulation Results

2.66%

Expected Annualized Return (Product)

19.05%

Probability of Negative Return

-28.96%

99% Confidence VaR (1 year)

| Metric | Structured Product | Underlying Benchmark |

|---|---|---|

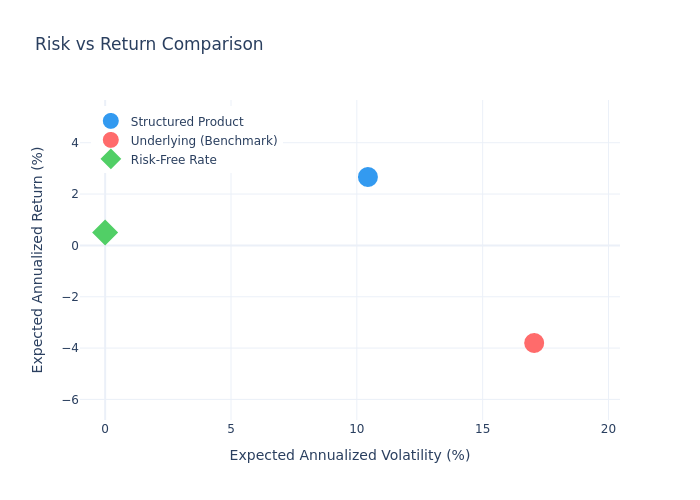

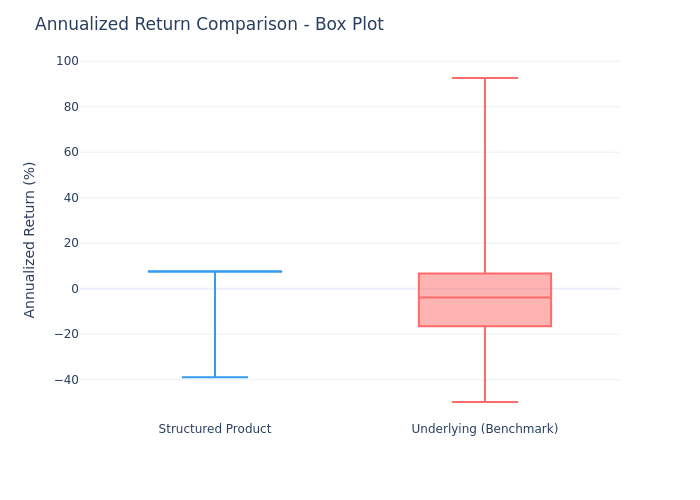

| Expected Annualized Return | 2.66% | -3.80% |

| Expected Annualized Volatility | 10.44% | 17.05% |

| Probability of Negative Return | 19.05% | 54.93% |

| 99% Confidence VaR (1 year) | -28.96% | -38.03% |

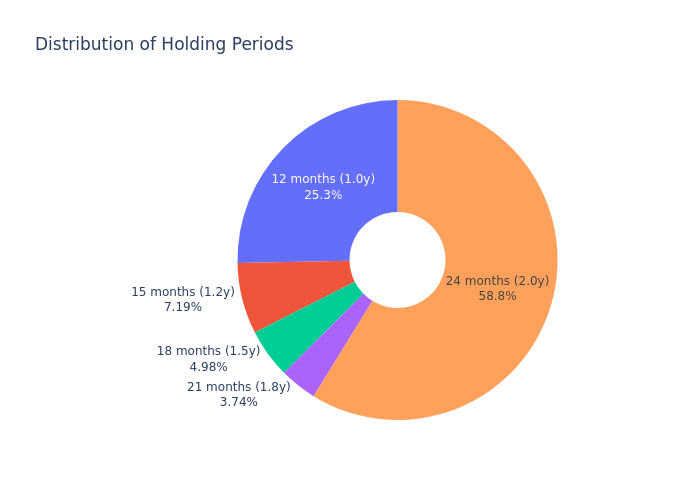

| Expected Holding Period | 1.66 years | — |

| Expected Total Return (over holding period) | 3.66% | -10.17% |

Basic Product Information

How It Works

This is a Barrier Reverse Convertible linked to a basket of three Swiss stocks: ABB Ltd, Alcon Inc, and UBS Group AG.

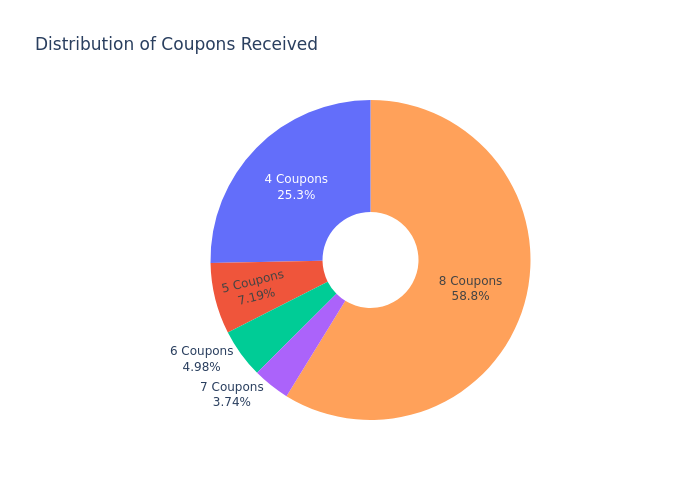

- Coupon Payments: The product pays a fixed quarterly coupon of CHF 19.25 (1.925% per quarter, 7.70% p.a.) regardless of the underlying performance.

- Barrier Protection: A 55% barrier is observed continuously. If none of the three underlyings ever trades at or below 55% of its initial level during the observation period, the investor receives full notional back at maturity.

- Downside Risk: If the barrier is breached and the worst-performing underlying is below its initial level at maturity, the investor receives a number of shares of the worst performer, equivalent to the underlying's final performance.

- Issuer Call: The issuer has the right to call (early redeem) the product quarterly starting after 12 months. If called, the investor receives full notional plus the coupon for that period.

| Parameter | Value |

|---|---|

| Product Type | Multi Barrier Reverse Convertible (SSPA 1230) |

| Underlyings | ABB, Alcon, UBS (worst-of payoff) |

| Currency | CHF |

| Coupon Rate | 7.70% p.a. (paid quarterly) |

| Barrier Level | 55% of initial (continuous observation) |

| Strike Level | 100% of initial |

| Tenor | 2 years |

| Issuer Call | Quarterly from month 12 onwards |

Charts

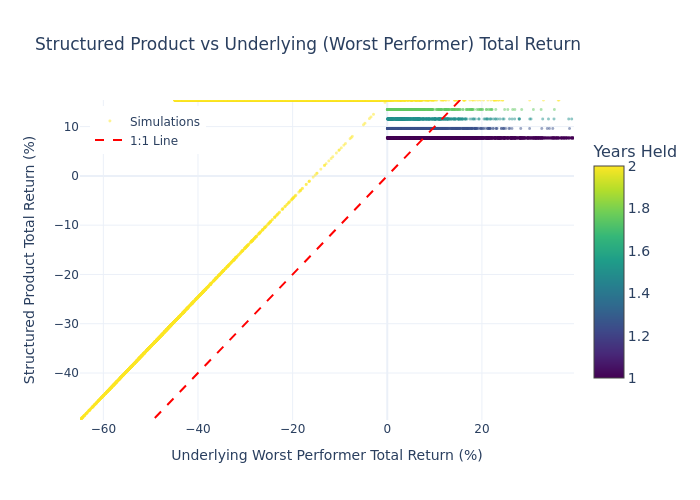

Scatter Plot: Product vs Underlying Returns

Each dot represents one simulation. The red dashed line is the 1:1 line. Simulations above the line mean the product outperformed the worst-performing underlying.

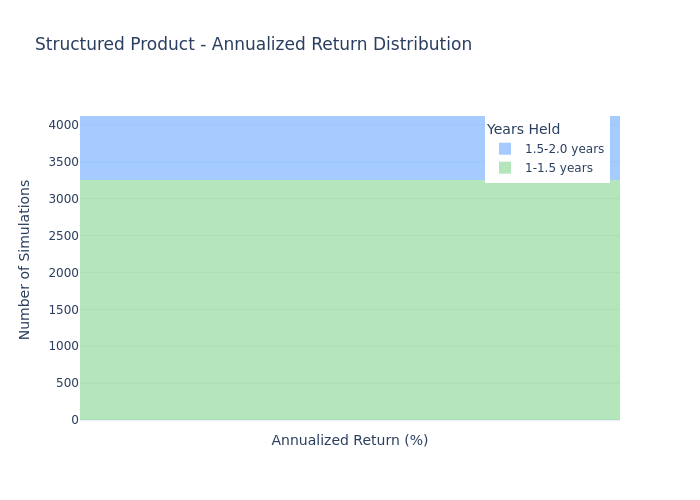

Annualized Return Distribution – Structured Product

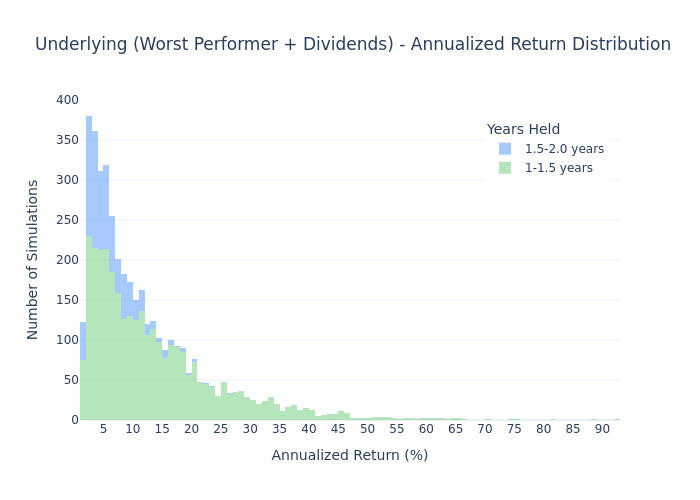

Annualized Return Distribution – Underlying (Worst Performer + Dividends)

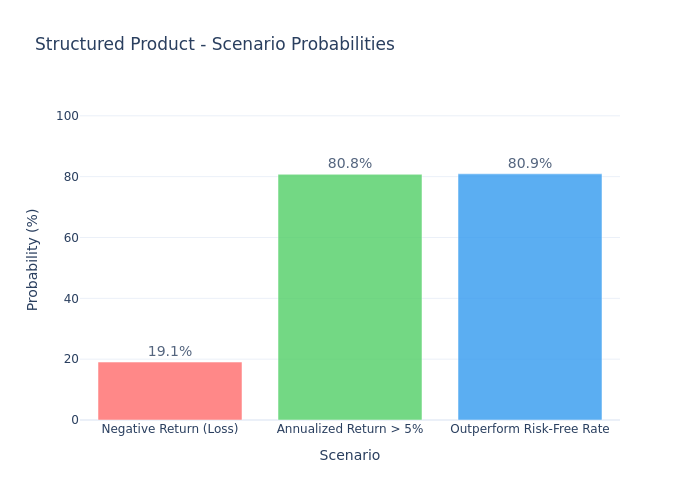

Scenario Probability Bar Chart

Risk vs Return Comparison

Box Plot Comparison

Holding Period Distribution

Distribution of Coupons Received

Key Statistics

Structured Product

| Statistic | Value |

|---|---|

| Expected Annualized Return | 2.66% |

| Median Annualized Return | 7.42% |

| Expected Annualized Volatility | 10.44% |

| Probability of Negative Return | 19.05% |

| 99% Confidence VaR (1 year) | -28.96% |

| Expected Total Return (over holding) | 3.66% |

| Expected Holding Period | 19.91 months |

| Probability of Early Redemption | 41.20% |

| Probability of Barrier Event | 19.79% |

Underlying Benchmark (Worst Performer + Dividends)

| Statistic | Value |

|---|---|

| Expected Annualized Return | -3.80% |

| Median Annualized Return | -3.89% |

| Expected Annualized Volatility | 17.05% |

| Probability of Negative Return | 54.93% |

| 99% Confidence VaR (1 year) | -38.03% |

Investment Commentary

Pros

- Attractive coupon: The 7.70% p.a. quarterly coupon is significantly higher than current CHF risk-free rates.

- Downside protection through barrier: The 55% barrier provides a substantial cushion before capital is at risk.

- Positive expected return: The structured product has a positive expected annualized return (2.66%) compared to the negative expected return of the worst-performing underlying (-3.80%).

- Reduced volatility: The product's annualized volatility (10.44%) is significantly lower than the underlying benchmark (17.05%), thanks to the coupon buffer and barrier protection.

- Low probability of loss: Only 19.05% of simulations resulted in a negative annualized return.

Cons

- Upside capped: Maximum annualized return is capped at 7.70% (the coupon rate), regardless of how well the underlyings perform.

- Worst-of structure: The product is exposed to the worst-performing of three stocks, which increases the probability of a barrier event and loss.

- Issuer call risk: The issuer can call the product early (41.20% probability), which would limit total coupon income.

- Credit risk: The product is unsecured and subject to the credit risk of the issuer (Leonteq Securities AG) and guarantor (Aargauische Kantonalbank).